Debt consolidation loans offer a way to lower your interest rates on multiple debts by combining them into one loan. As any financial planner will tell you, one of the trickiest parts of managing your money is dealing with multiple creditors. Juggling your credit card balance, consumer debts, mortgage and more can be confusing, and chances are good you’re not getting the lowest interest rate possible.

Banks, credit unions and installment lenders can offer debt consolidation loans. These loans simplify the number of times you have to make payments by converting many of your debts into one loan payment. These offers may have a lower interest rate than what you are currently paying.

If you've ever wondered what a debt consolidation loan is and how it works, it's time for a bank, credit union, or finance company to lend and "consolidate" (bring it all together) money to pay off outstanding credit card debt. with one big loan. This is the definition of debt/account consolidation in the simplest terms.

Someone usually applies for a consolidation loan when they have difficulty paying the minimum monthly payment. There are many advantages and disadvantages to obtaining such a loan, as well as several requirements that must be met in order to obtain a loan.

A debt consolidation loan pays off your debt because the lender lends you the money you need to pay off your existing debt. For example, if you have three credit cards and owe a total of $20,000, ask your lender for a consolidation loan and they will give you $20,000 if you qualify.

Then they will typically pay off your existing credit cards with the money, close those credit card accounts, and have you make one monthly payment to them for the $20,000 you borrowed.

Unfortunately, what can happen is that if you don’t have a realistic household budget that you actively use, you’ll be struggling again and reapplying for new credit cards after a few months of making personal loan payments. When this happens, you can actually end up doubling your debt rather than paying it off with a consolidation loan.

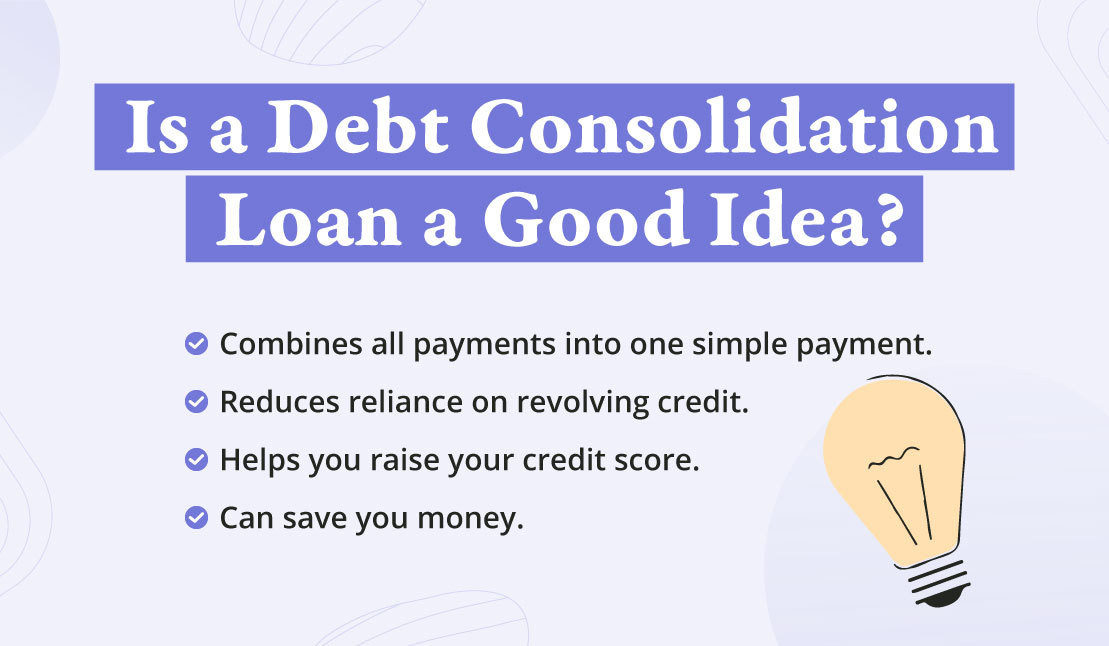

The main advantage of a debt consolidation loan is that your current debt is paid off. Those credit cards that you’ve been struggling to pay, household bills, and even overdrafts on your bank accounts.

An unsecured debt consolidation loan can relieve you of the burden of paying various bills each month, including overdue bills. Other benefits include:

Lenders are cautious when approving unsecured debt consolidation loans. To qualify for one of these, you generally need to have a solid income, a high net worth (worth of your assets after all debts have been deducted), a very high credit score, or a surety with a very high net worth. A very strong credit score. Other disadvantages include: